Budgeting is key to a solid personal finance strategy.

No matter how much you earn, you should create a budget to know how to spend your money and create a savings plan.

Creating your first budget is a major step to getting your finances under control, starting to pay off debt, and avoiding mistakes that might slow you down.

If you have never created a budget, this step can feel overwhelming.

But don’t worry, I have your back.

This blog post will give you everything you need to create your first budget.

Let’s dive in!

Pin for Later 📌

How to Create A Budget You Will Stick To

1. Know Your “Why”

Budgeting can be quite time-consuming in the beginning.

You will have to make an effort to adopt new habits and be conscious about your money.

If you are creating your first budget, several concepts will probably be new to you. Hence, budgeting can be overwhelming at first.

This is why having a clear motivation is key to staying focused. If you already have a budget but want to improve it to live by it, you will find valuable advice in this post.

Knowing your “why” is essential to motivate yourself in both cases.

Before creating your budget, ask yourself why you need to do it.

Are you willing to pay off debt as fast as possible? Or maybe you are trying to save for your dream wedding?

No matter why you decide to start budgeting, having a clear goal in mind will make this process more motivating and rewarding.

So think about it, know why you are doing it, and set some goals!

2. Choose The Right Format For You

Choosing the proper format is the first step to creating the right budget for you.

Once your budget has been created, you should not need to make significant changes to it.

Hence, you need to find a format you will be comfortable with.

I use Excel as it is a powerful tool offering many functionalities, but I know many people who rather have their budgets in a notebook.

Budgeting apps are a 3rd option.

You might prefer this format if you want to keep your budget with you at all times or check your expenses on the go.

If you want to use an app to create your budget, you might consider trying the following ones :

- Mint is often considered the best app on the market for creating budgets, tracking bills, and giving you an overall picture of your wealth. To use the app, you need to connect your bank accounts, loans, and investments to get an overview of your finances. Just like the next app on the list, Mint is completely free to use, which is a really big plus if you are not sure apps are the way to go to create your first budget.

- Honeydue: Honeydue is a great app to budget as a couple. It allows you to create a budget, track expenses, and share the information in real-time with your partner. This app will give you a great overview of your expenses and respective bank accounts. Just as for the other apps on the list, Honeydue can help you have an overview of your financial situation and expenses by synchronizing your accounts and cards. Honeydue is completely free to use. It relies on tips, so if you enjoy the app, do not hesitate to send the developers a little something.

- YNAB (You need a budget): YNAB is an app based on an educational approach. You will have to allocate every single dollar you make and give it a purpose. The app won’t let you budget more than what you are making, forcing you to create a realistic budget. You will also get valuable advice to help you to live within your means. The educational e-mails you will receive from the team are really a plus to help you gain knowledge on personal finance. Just as for Mint, YNAB offers you a real-time overview of your finances thanks to the automatic synchronization of your cards and accounts. The basic functionalities of the app are free, but you can upgrade your account to unlock the advanced features. This premium account will cost you 84$ a year.

- EveryDollar: Dave Ramsey is the brain behind the EveryDollar app. This app is great for beginners willing to create their first budget. EveryDollar is a great app to have a quick overview of your finances. Users have to enter their income and monthly expenses to create an easy budget. They can also link their bank accounts, which will automatically synchronize expenses. Unfortunately, to do so, a premium account is necessary. This premium account will cost you 99$ a year.

Since Mint and Honeydue are free, if you are willing to give budget apps a try, you might want to start with one of these.

3. Know Exactly How Much You Make

Now that you have decided in which format you will make your budget, we can start talking about figures.

If you only have one source of income, this part will be easy.

You need to have a look at your paychecks to know precisely how much you make every month. If you have several sources of income, you will have to add them all to figure out how much you have to go around every month.

If your income varies from one month to another, track the changes and update this section every month.

4. List Your Monthly Expenses

Listing all your monthly expenses is at the core of creating a budget.

You need to make sure not to forget any bills.

How you decide to address this part of your budget will depend on several things:

- Are you paid once a month or every two weeks?

- Does your salary vary from one month to another?

- Do you have any cash bonuses?

Although some of your expenses are to be paid annually, you should budget for them monthly.

The money allocated to these periodical expenses can be wired to a separate bank account at the end of the month.

Once you receive the bills, pay them using the money set aside.

This fund is called a sinking fund.

Breaking down these expenses into monthly payments is definitely a good initiative, as it adds more security to your finances.

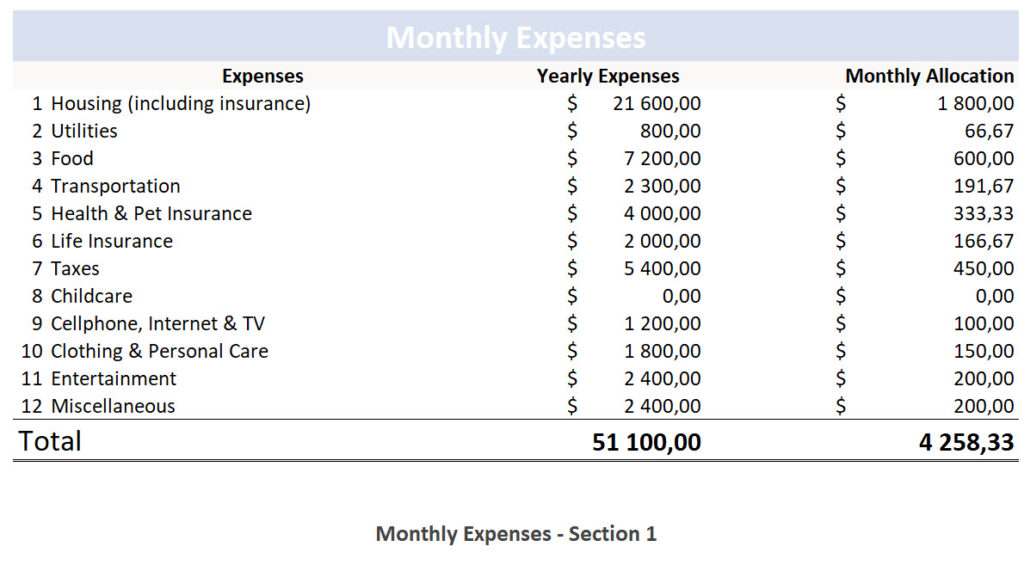

The monthly expenses to add to your budget include :

- Housing

- Utilities

- Food

- Transportation

- Health/pet insurance

- Life insurance

- Taxes

- Childcare

- Cellphone, cable TV, and internet

- Clothing and personal care

- Entertainment

- Miscellaneous

According to Dave Ramsey’s theory, the first four elements of this list are known as the four walls.

When times are tough and your budget is tight, these four elements should be your priority.

I would also include Health and pet insurance in these top priorities because we all know how expensive treatments can be.

At this point, your budget should look like this :

The table above is just an example based on experience. The amounts will vary based on the country you live in and based on your lifestyle.

If you live in the US and need help defining how much you should allocate to each category, you can find Dave Ramsey’s percentages here.

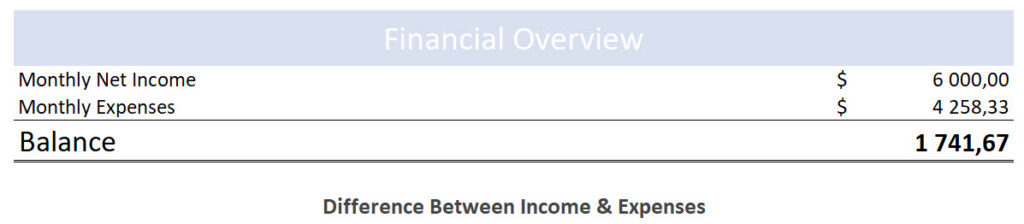

You might have noticed that debts, except for the mortgage, are not included in the first part of the budget. The idea is to treat them separately after calculating the total of your monthly expenses.

Once you have done the math and know how much your monthly expenses cost you, you can subtract that amount from your total income.

This calculation will tell you how much you can save and allocate to debt payoff.

5. Decide How Much You Want to Save

Before we discuss the trickiest part of the budget—debt—you need to consider your current savings.

You probably already know that you should have an emergency fund equal to at least half a salary and a survival fund equal to about three to six months’ income.

If you haven’t started saving yet, you should consider it. Saving will offer you financial security. It will help you cope with unexpected expenses and avoid further debt. Hence, if you haven’t enough savings yet, you will have to decide how much you want and can save.

Many people decide not to start saving before they have fully paid off their debt. This is really up to you, but as it will probably take several months, or even years, to fully pay off your debt, you are definitely taking a risk if you decide to go with this strategy.

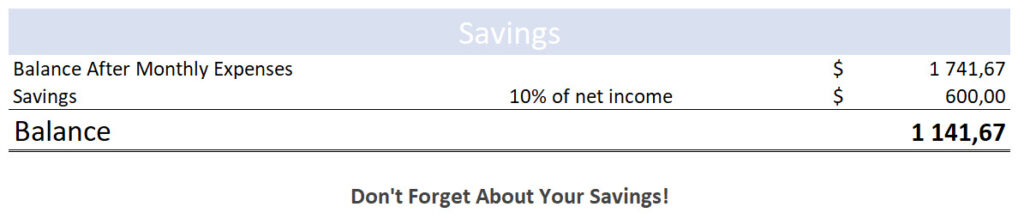

For this exercise purpose, let’s say you want to save 20% of the money you have left after paying for your monthly expenses:

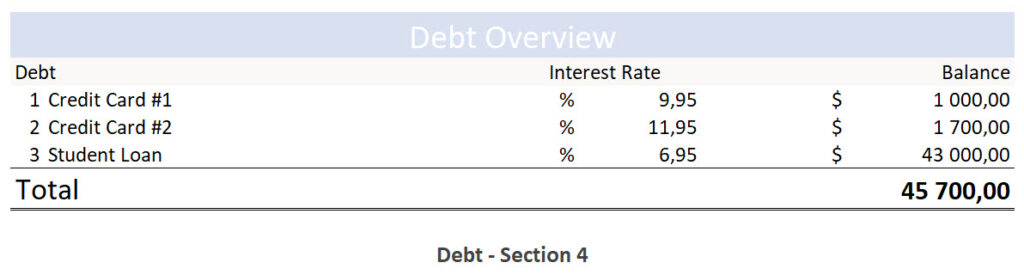

6. List Your Debt

Listing your debt (except your mortgage) is one of the most important parts of your budget. You should know exactly how much you owe.

List your debts and their monthly minimum payments. At this point, you should have an overview of your debts to decide which debt payment method to choose.

After listing your debt, do you notice important differences between their respective interest rates? Does any of your debts have outrageous interest rates? If so, you might want to start paying off these debts first.

If all your debts have similar interest rates, you might instead start paying off your debt, starting with the smallest balance.

These two methods are called the Avalanche (paying the highest interest rate first) and the Snowball (paying the smallest balance first).

The idea is to pay the minimum payments on all positions except for the first one. You want to put as much money as possible towards paying off this position.

At this point, you need to decide which method to use, as it will impact the structure of the rest of your budget. Keep in mind that you should stick to a method until your debt is fully paid off.

7. Implement Your Strategy

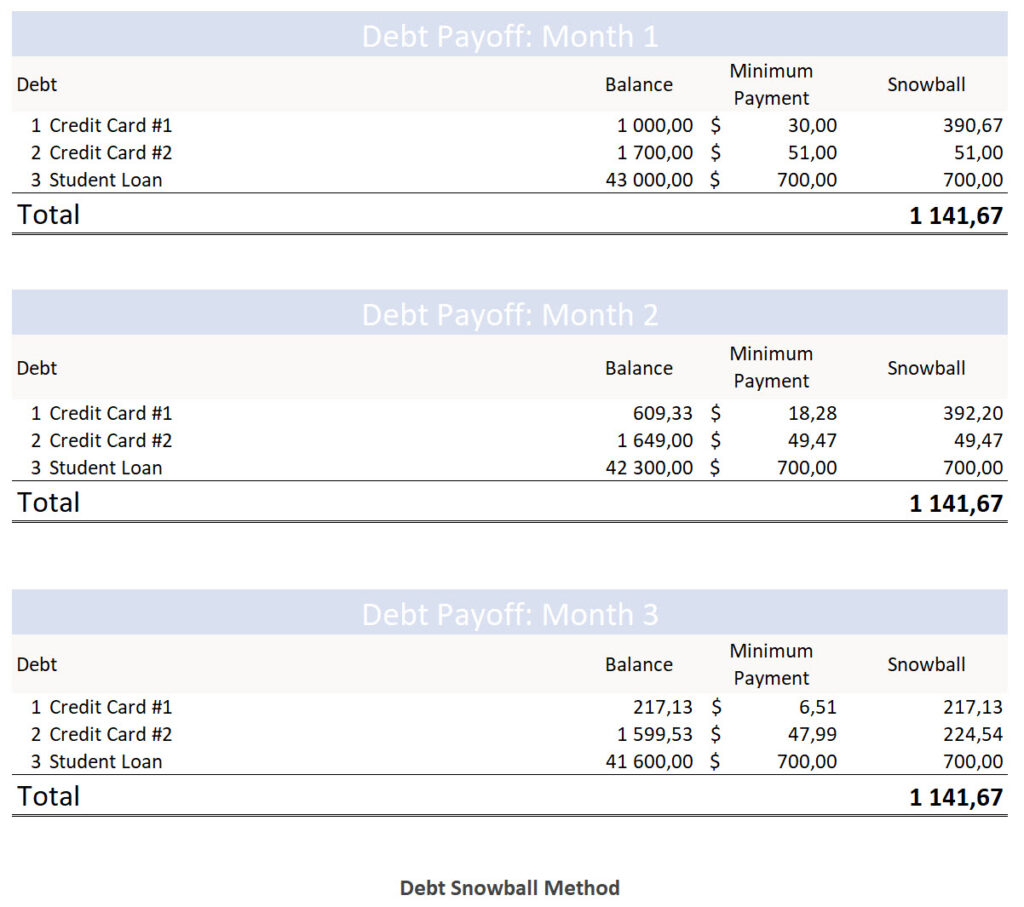

Now that you know how much you have left after paying your monthly expenses and savings, you need to define how to allocate the remaining money to your debt pay-off.

In this example, your monthly income is 4500$. After calculating your monthly expenses, you have 1300$ left for debt pay-off and savings.

You decided to save 20% ($260) of that amount, which leaves you with $1040 to allocate to your debt pay-off.

You have decided to use the Debt Snowball method. It is the most common method, so let’s assume this strategy suits your situation…

This part of your budget should look like this:

The debt Snowball method is pretty straightforward.

Once you have fully paid off the smallest balance, allocate as much money as possible to pay off debt n°2 while paying the minimum payments on all the other balances.

Start again until all of your debts are fully paid off.

8. Live by Your Budget

Now that you have created a realistic budget, you need to live by it. This means avoiding overspending and temptation.

If you are used to carrying credit cards, you might consider leaving them at home. Having cash is also a great way to avoid overspending.

Research shows that people spend more when they pay with a card. They can even spend up to 100% more when paying with a credit card! So do yourself a favor and leave these credit cards in a separate wallet at home.

Another simple way to save money is to unsubscribe from your favorite stores’ newsletters. Avoiding temptation is key to not overspending.

Lastly, you can also try the cash envelope system. This system is pretty easy to use, as it simply implies separating the money allocated to the different categories in your budget.

In this example, 12 categories were used. This means that you will need to put your cash into 12 separate envelopes.

The money you have in one envelope is the money you can spend in this category until the end of the month. Once an envelope is empty, you can no longer spend money in this category.

9. Reflect Regularly

Although you should not need to make significant changes to your budget every month, you need to remember that budgeting is a process.

This is not something you can do once a year and then forget about.

You should take time to reflect on your spending and adapt your budget every month when paying your bills.

You need to reflect to make sure your budget suits your needs and is helping you improve your financial situation without making you feel miserable.

Update your budget every time a change occurs to keep it as realistic as possible. Your rent might increase, or you might decide to get cheaper insurance. Keeping track of these changes is important to keeping your budget accurate.

10. Keep Learning

To live by your budget, you will need to make some lifestyle changes.

You will, for instance, need to start tracking your spending and will probably want to try different methods and tools.

You need to be ready to learn and implement new strategies when it comes to lifestyle changes. Budgeting will quickly become a game allowing you to save money.

And you will quickly realize that there are a ton of ways to save money on a daily basis. All you need to do is keep learning and apply what you’ll learn along the way.

Final Thoughts

Whether you are a beginner or a pro, budgeting implies work and dedication.

If you are new to this, remember that budgeting implies a few changes in your behavior (such as tracking expenses, keeping receipts, and looking for cheaper alternatives).

Give yourself the necessary time to get comfortable with budgeting. If you have never paid attention to your spending, you will not be able to master budgeting overnight. Creating the perfect budget takes time.

You will be able to adapt your budget to make it drastically improve your finances. You will rapidly catch yourself looking for better deals and ways to decrease spending. This is a slow process, but you will get there.

Budgeting should not be a pain. To be effective, it needs to become a habit.

So make it fun and enjoy your progress!